HCM Insights

The third quarter of 2025 tested investors’ discipline amid narrowing leadership and rising valuation dispersion. With the AI hyperscalers continuing to dominate index-level returns, many income-oriented portfolios struggled to keep pace. Yet the Hilton Dividend & Yield Strategy (DIVYS) again demonstrated its ability to compound steadily through uneven markets, delivering a +7.03% gross (+6.88% net) third quarter return versus +5.90% for the Nasdaq U.S. Dividend Achievers benchmark, an excess of +113 bps.

Performance was led by tactical reallocations from late Q2 and early Q3 that favored industrial enablers, energy infrastructure, and global financials, each supported by durable dividend growth and valuation headroom. The portfolio remains deliberately balanced between secular growth exposure (semiconductors, automation, and connectivity) and stable cash compounders (financials, utilities, and staples). While broader equity markets appear increasingly momentum-driven, we continue to find selective opportunities in high-return, cash-generative franchises whose fundamentals remain under-appreciated by passive dividend indices.

Macro and Market Backdrop

The third quarter featured a tug-of-war between moderating inflation and persistent fiscal expansion.

- Rates & Inflation. The 10-year Treasury yield nearly touched 4.5% in August before retreating as inflation data softened. Core PCE decelerated but remained above the Fed’s comfort zone at >2.8% YoY, keeping monetary policy biased toward “higher for longer.”

- Fiscal & Growth. Fiscal deficits remain near 7% of GDP, sustaining issuance pressure and reinforcing the higher-for-longer narrative. Economic growth cooled modestly as consumer strength waned and the labor market normalized.

- Equities & Leadership. Index gains were once again narrowly concentrated in a handful of AI beneficiaries, even as cyclical sectors such as Industrials and Financials began to recover late in the quarter. Dividend payers broadly lagged the S&P 500 but outperformed on a risk-adjusted basis, benefiting from lower volatility and steadier earnings growth.

This environment rewarded capital discipline: yield visibility and margin resilience proved more valuable than chasing headline AI multiples.

Strategy Performance and Positioning

DIVYS’ outperformance for the third quarter stemmed from stock selection in Industrials, Energy, Information Technology, and Communication Services, while disciplined single-name specific trims protected capital from broader factor rotations.

- Sector Allocation. Industrials (+215 bps contribution) and Energy (+87 bps) led gains, driven by exposure to TE Connectivity (TEL), Analog Devices (ADI), Williams (WMB), and General Dynamics (GD).

- Stock Selection. AI enablers such as Taiwan Semiconductor (TSMC) and TEL delivered double-digit returns as datacenter and automation demand continued to scale.

- Financials. Active adds to Wells Fargo (WFC), Truist (TFC), and Bank of America (BAC)benefited from curve steepening and resilient credit metrics.

- Defensive Yielders. Exiting Coca-Cola (KO) and reallocating to higher-growth, yield-accretive names lifted the portfolio’s forward dividend yield to 2.23% while enhancing duration neutrality.

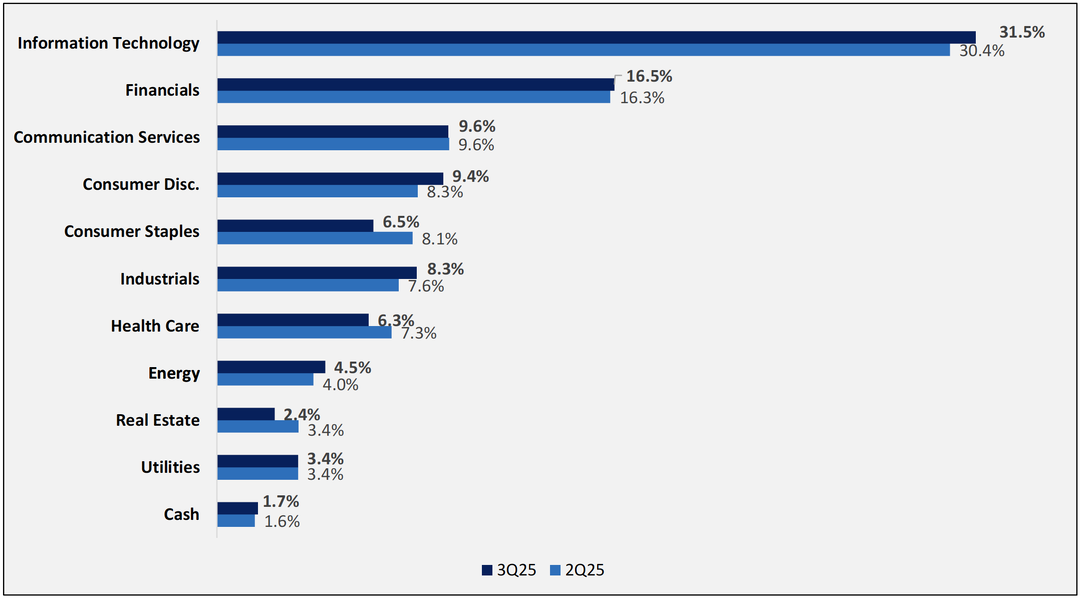

Figure 1: DIVYs 3Q25 v. DIVYs 2Q25 Sector Weights

Figure 1: DIVYs 3Q25 v. DIVYs 2Q25 Sector Weights

Source: Bloomberg & INDATA

At quarter end, the portfolio maintained a beta of 0.88, a 1-year standard deviation of 14.6% (vs. 18.7% for the S&P 500), and remained overweight Information Technology, Financials, and Industrials.

Relative Performance and Peer Comparison

While the Hilton Dividend & Yield Strategy is benchmarked to the Nasdaq U.S. Dividend Achievers Index, its risk-adjusted results have also stood out against both the broader market and the largest dividend-focused ETFs.

Through September 30th, DIVYS gained +15.4% gross/ +15.0 net year-to-date, outperforming the S&P 500 (+14.8%) and the Nasdaq U.S. Dividend Achievers benchmark (+12.28%), despite underweighting the S&P 500’s ultra-high-beta AI leaders. Against peer dividend strategies, DIVYS' advantage was even more pronounced: gross performance outperformed the popular Schwab US Dividend Equity ETF (SCHD) and the S&P 500 Dividend Aristocrats ETF (NOBL) by approximately +1,250 bps and +1,000 bps, respectively, over the same period.

We believe that this consistency underscores DIVYS' defining edge, quality yield without concentration risk. Whereas SCHD and NOBL remain heavily tilted toward legacy Industrials, Financials, and Energy, DIVYS maintains a more balanced exposure profile emphasizing Information Technology (~31%), Communication Services (~10%), and Industrials (~8%), sectors driving both dividend growth and earnings momentum.

Dividend durability remains a core differentiator: the strategy’s forward yield of 2.2% is paired with three-year dividend growth exceeding peers by nearly 200 bps annually, signaling a healthier blend of current income and reinvestment capacity. The result is a strategy that has captured much of the equity market's upside while preserving a low-volatility profile — a rare combination in a year dominated by narrow leadership.

Put simply, the data shows that DIVYS has achieved what many dividend strategies have not: market-level returns without speculative concentration, making it a compelling solution for investors seeking steady compounding, credible income growth, and disciplined risk management.

Portfolio Adjustments*

July — Repositioning for AI Durability and Yield Efficiency

Early in the quarter we exited Coca-Cola (KO) and trimmed Accenture (ACN) to reduce exposure to structurally challenged cash-flow models. The KO sale reflected our view that surging GLP-1 adoption is structurally eroding demand for calorie-dense beverages just as pricing power fades, leaving the shares rich relative to peers. The ACN trim partially neutralized our exposure to the utilization-based consulting model, which faces AI-driven commoditization and margin pressure.

Proceeds were redeployed into higher-conviction compounders aligned with durable industrial and AI infrastructure demand. We increased Analog Devices (ADI), TE Connectivity (TEL), and Taiwan Semiconductor (TSMC), each a direct beneficiary of the recovery in analog semiconductors, automation, and data-center build-out. We also initiated a 1% position in Lennar (LEN), a contrarian re-entry into homebuilders as stabilizing mortgage spreads and moderating supply create asymmetric upside potential.

August — Expanding Global Industrial Diversification

We initiated Siemens AG (SIEGY) to broaden our exposure to electrification, automation, and industrial software while maintaining our quality-income bias. The position complements existing holdings in TEL and ADI and adds geographic diversification to the European industrial base. To fund this rotation, we modestly trimmed Amgen (AMGN), AstraZeneca (AZN), and AbbVie (ABBV) following strong performance and limited near-term catalysts within healthcare.

September — Shifting Toward Energy Infrastructure and Financials

In September we completed the exit of Accenture (ACN), reallocating proceeds to Williams Companies (WMB), where accelerating AI-related power demand supports long-duration volume growth and a durable dividend. Later in the month, we monetized American Healthcare REIT (AHR) after a significant re-rating (~26× AFFO) and rotated into large-cap banks, Wells Fargo (WFC), Truist Financial (TFC), and Bank of America (BAC). With funding costs poised to ease and net-interest margins improving, these franchises offer more compelling dividend coverage and total-return visibility than premium-valued REITs.

*The portfolio adjustments listed above include all transactions in the strategy for the quarter.

Quick Snapshot of 3Q25 Attribution

- Quarter end allocation to cash was down at 1.68% as cash was used to fund new positions.

- Yield on the portfolio as of 09/30/2025 was 2.07% and the 1-year Beta was 0.92.

- The Dividend and Yield Strategy returned +7.03% gross (+6.88% net) for 3Q 2025, which was 113 bp ahead of the benchmark** return.

- Relative to the Nasdaq US Broad Dividend Achievers (DAATR), DIVYS was overweight Information Technology, Consumer Discretionary, Communication Services, Energy, and Real Estate.

- Relative to the Nasdaq US Broad Dividend Achievers (DAATR), DIVYS outperformed in Information Technology, Communication Services, Consumer Discretionary, Real Estate, and Energy in 3Q25.

- For 3Q25, top single-name contributors included Corning (GLW), TSMC (TSM), TE Connectivity (TEL), Oracle Corp. (ORCL), Communication Services Sector SPDR ETF (XLC), Fidelity MSCI Consumer Discretionary ETF (FDIS), TJX Companies (TJX), American Healthcare REIT (AHR), Utilities Selector Sector SPDR ETF (XLU), British American Tobacco (BTI), Xylem Inc. (XYL), Itochu Corp. (ITOCY), General Dynamics (GD), AstraZeneca (AZN), Quest Diagnostics (DGX), and Truist Financial (TFC).

- For 3Q25, top single-name detractors included Intercontinental Exchange Inc. (ICE), Ares Management (ARES), Philip Morris International (PM), Darden Restaurants Inc. (DRI), and Accenture (ACN).

- The DIVYS Strategy continues to maintain a low standard deviation versus the market– one-year standard deviation of 14.6% vs. benchmark of 15.2% and S&P 500 of 18.7%

Outlook

As we enter the final quarter of 2025, we see the macro landscape continuing to be defined by high nominal growth, sticky inflation, and constrained fiscal headroom. For dividend investors, this environment rewards cash efficiency, companies that can self-fund growth, sustain dividend growth, and reprice their value proposition amid tighter capital conditions.

We continue to favor:

- AI Enablers with capital-light models and recurring free cash flow (TSMC, ADI, TEL).

- Financial Compounders benefiting from a steepening curve (WFC, TFC, BAC, BLK).

- Energy Infrastructure with inflation-linked cash flows (WMB).

- Global Industrials with multi-cycle durability with AI growth optionality (SIEGY, GD, EMR).

Valuation and volatility discipline remains paramount. Dividend quality, not yield for yield’s sake, will continue to drive long-term compounding. We believe that DIVYS enters the fourth quarter positioned to participate in further market broadening while preserving its defining characteristics: low volatility, high visibility, and a consistent bias toward shareholder yield.

**Benchmark: NASDAQ US Broad Dividend Achievers

Important Disclosures:

Hilton Capital Management, LLC (“HCM”) is a Registered Investment Advisor with the US Securities Exchange Commission. The firm only transacts business in states where it is properly notice-filed or is excluded or exempted from registration requirements. Registration as an investment advisor does not constitute an endorsement of the firm by securities regulators nor does it indicate that the advisor has attained a particular level of skill or ability.

The views expressed in this commentary are subject to change based on market and other conditions. The document contains certain statements that may be deemed forward looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. Sources include Bloomberg and INDATA (our portfolio accounting and performance system). There is no representation or warranty as to the current accuracy, reliability, or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

The performance information contained herein is unaudited, was calculated by HCM and is shown on both a gross-of-fee and net-of-fee basis. The performance results herein include the reinvestment of dividends and/or other earnings, and the net-of-fee performance results are shown net of the actual advisory fees paid by the client accounts in the HCM Dividend & Yield Composite. In addition, actual client accounts may incur other transaction costs such as brokerage commissions, custodial costs and other expenses. Accordingly, actual client performance will differ, potentially materially, particularly given that the net compounded impact of the deduction of investment advisory fees over time will be affected by the amount of the fees, the time period, and the investment performance. For additional information about the composite, please contact us - info@hiltoncm.com

All investing involves risks including the possible loss of capital. Asset allocation and diversification do not ensure a profit or protect against loss. Please note that out- performance does not necessarily represent positive total returns for a period. There is no assurance that any investment strategy will be successful. All investments carry a certain degree of risk. Dividends are not guaranteed, and a company’s future ability to pay dividends may be limited.

Additional Important Disclosures may be found in the HCM Form ADV Part 2A, which can be found at https://adviserinfo.sec.gov/firm/summary/116357.