HCM Insights

The second quarter of 2026 was a strong absolute-return period for the Hilton Tactical Income Strategy. The Hilton Tactical Income Composite generated a preliminary return of 4.59% gross /4.46% net, participating meaningfully in the recovery across equities, credit, AI infrastructure, energy infrastructure, and global dividend-oriented exposures. The benchmark* returned +6.24%, resulting in relative strategy underperformance of approximately 165 basis points for the quarter.

While we are always focused on improving relative results, we believe the quarter’s attribution requires important context. Tactical Income is not an unconstrained 40/60 portfolio. Every holding in the strategy must contribute to the portfolio’s income and volatility profile, which naturally limits exposure to many of the highest-volatility, non-yielding or very low-yielding benchmark* constituents. That distinction mattered meaningfully in 2Q26, as a significant portion of the benchmark’s performance came from names such as Micron, Advanced Micro Devices, Intel, Sandisk, Amazon, and Tesla, securities that either do not fit the strategy’s yield framework or would not be sized in the portfolio in the same way they are represented in the benchmark*.

In fact, these benchmark-only or structurally difficult-to-own positions accounted for more than the total relative shortfall during the quarter. Micron alone detracted approximately 62 basis points from relative performance, while Advanced Micro Devices, Intel, Sandisk, Amazon, and Tesla together represented an additional meaningful drag. Viewed through that lens, we believe the strategy had a solid quarter. The strategy generated, what we feel, is a strong positive absolute return, maintained its income discipline, and participated in several key market themes through yield-eligible holdings such as NVIDIA, Applied Materials, Cisco, Caterpillar, Taiwan Semiconductor, Alphabet, Broadcom, Alerian MLP ETF, and Williams.

The quarter therefore highlights both the strength and the constraint of the Tactical Income framework. In a momentum-led market where the benchmark* is rewarded for owning non-yielding growth and high-beta technology exposures, the strategy may lag on a relative basis. However, we believe the portfolio performed well within its mandate: generating income, participating in upside, maintaining diversified exposure, and avoiding a wholesale shift into securities that do not meet the strategy’s income objective.

Average exposures during the quarter were approximately 47.3% equity, 49.2% fixed income, 2.3% cash, and 1.2% commodities, compared with benchmark* averages of roughly 40% equity and 60.0% fixed income.

Macro & Market Landscape

The second quarter was defined by a rapid shift from macro caution to renewed risk appetite. Entering the quarter, markets were still digesting elevated geopolitical risk, sticky inflation, and uncertainty around the direction of monetary policy. As the quarter progressed, geopolitical concerns eased, equity breadth improved, and the market increasingly rewarded companies tied to AI infrastructure, semiconductors, memory, power, industrial capex, and global reflation.

Inflation remained central to portfolio construction during the quarter. Early in 2Q26, we were focused on the risk that geopolitical tension and energy-market disruption could feed into a more stagflationary backdrop. That view supported exposure to real assets and energy-linked income streams, including incremental allocations to MLP exposure and ExxonMobil.

At the same time, the rate backdrop became less supportive for passive duration. Early in the quarter we reduced exposure to longer-duration fixed income and intermediate government exposure, while increasing shorter-duration investment grade credit, AAA CLO exposure, and diversified securitized credit. The objective was to maintain portfolio carry while reducing sensitivity to a scenario in which inflation remained stickier and the Fed had less flexibility to cut rates.

Late in the quarter, after having materially reduced duration risk, we modestly rebuilt intermediate credit exposure in the strategy. This was not a major directional shift, but rather a risk-balancing trade intended to bring the fixed income allocation somewhat closer to the benchmark* after a period of meaningful duration reduction.

Equities and Market Leadership

As mentioned, equity leadership broadened during the quarter, but not evenly. The strongest areas of the market were increasingly tied to AI infrastructure, semiconductors, memory, networking, power, and data-center-related capex. This supported several strategy holdings, including NVIDIA, Applied Materials, Cisco, Caterpillar, Taiwan Semiconductor, Alphabet, and Broadcom.

However, the strategy’s income mandate created a meaningful relative headwind. Several of the benchmark’s* strongest contributors were non-yielding or very low-yielding companies that Tactical Income either could not own, could only own in limited size, or accessed indirectly through lower-volatility, income-generating vehicles. This was most visible in Information Technology, where benchmark* exposure to higher-beta semiconductor and memory names significantly outpaced the strategy’s yield-constrained technology exposure.

Credit and Liquidity

Credit positioning in the strategy remained intentionally high quality. Rather than reach for yield through lower-quality spread products, we emphasized investment grade credit, short-duration credit, AAA CLOs, securitized credit, and cash equivalents. This helped preserve flexibility while still supporting the strategy’s income objective.

The strategy also used liquidity actively. Early in the quarter, ultra short- term US Treasury exposure was trimmed to fund higher-conviction equity and income opportunities as geopolitical risk appeared to ease. Later, we continued to balance liquidity, yield, and duration as the opportunity set evolved. We believe this flexibility remains one of the key advantages of the Tactical Income framework.

2Q26 Strategy Actions and Positioning

We believe that strategy activity during the quarter can be understood categorized in three phases: an early-quarter re-risking as geopolitical pressure eased, a mid-quarter rotation toward shorter-duration income and AI infrastructure exposure, and a late-quarter emphasis on valuation discipline and portfolio volatility control.

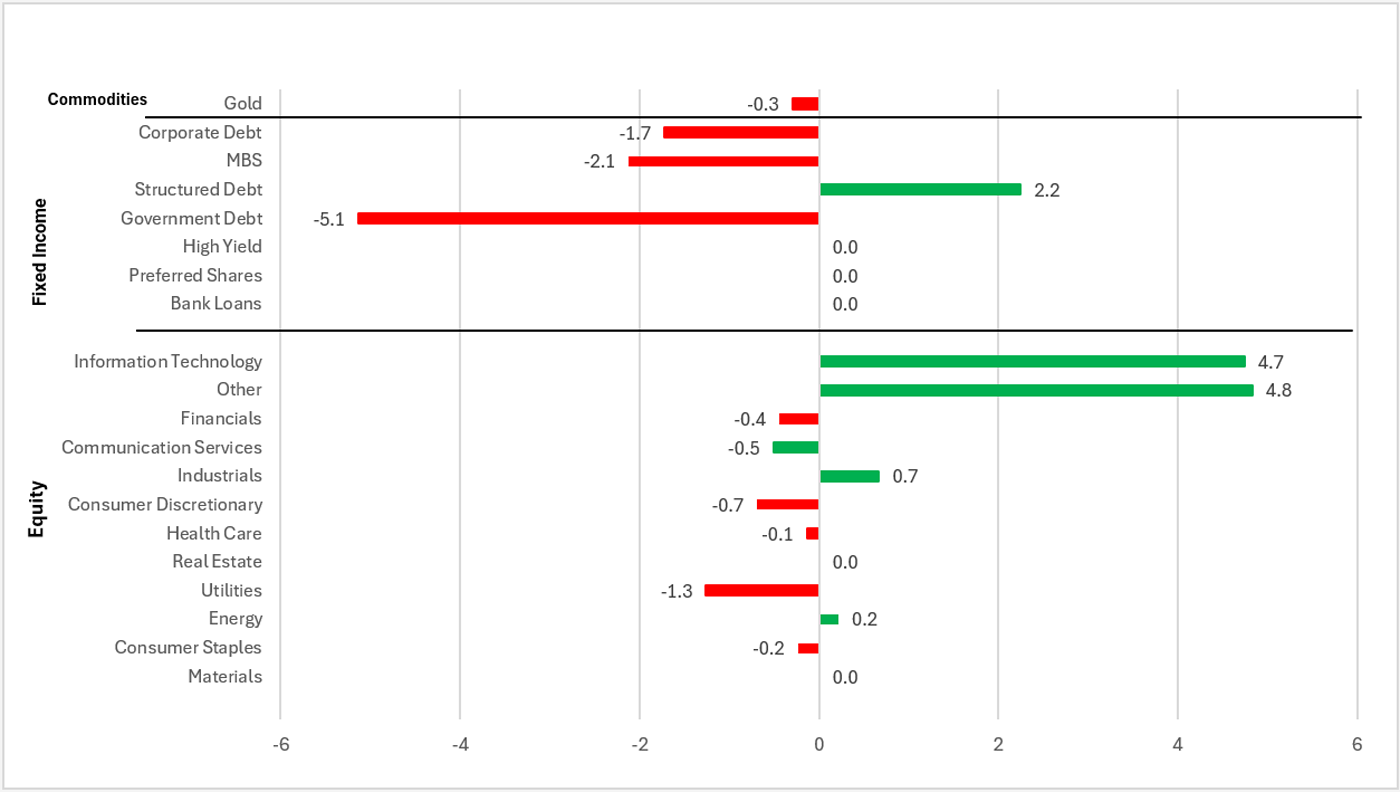

Figure 1: Tactical Income 2Q26 Sector Allocation Changes

Figure 1: Tactical Income 2Q26 Sector Allocation Changes

Source: Bloomberg as of 6/30/26

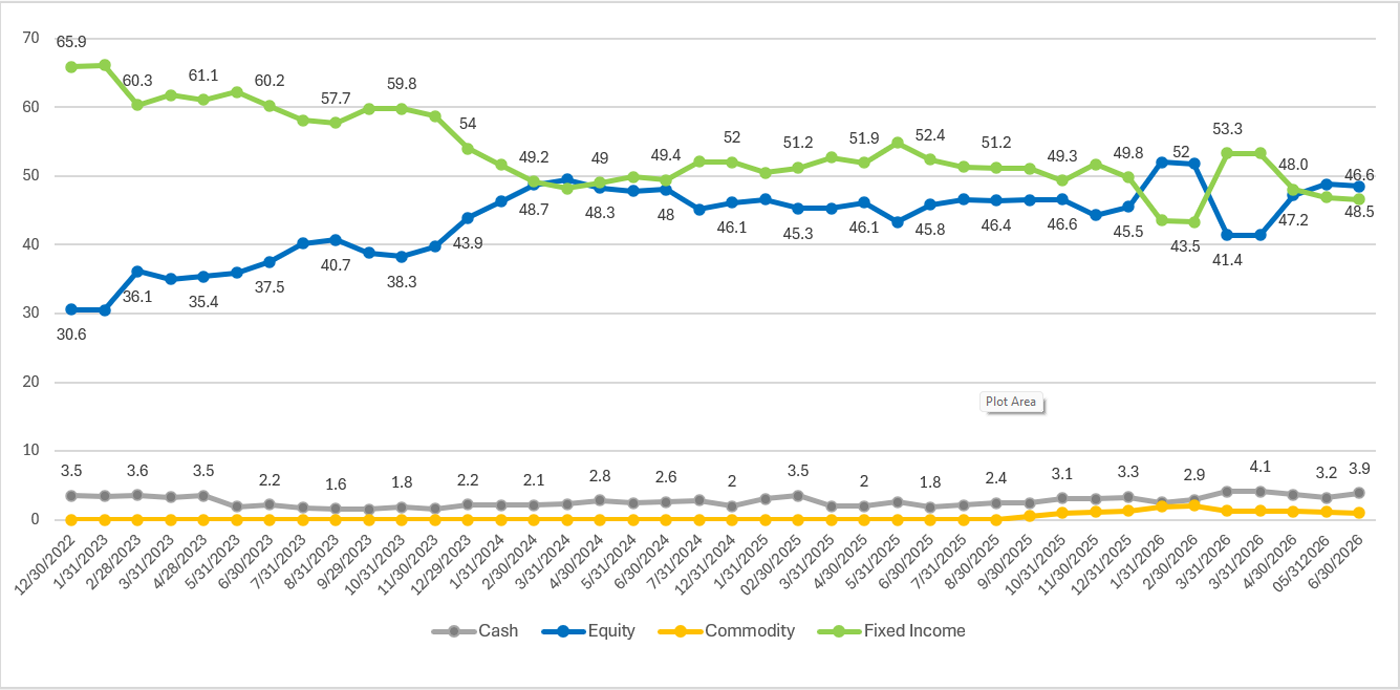

Figure 2: Tactical Income Asset Allocations

April 1st, 2026 – June 30th, 2026.

Figure 2: Tactical Income Asset Allocations

Source: Bloomberg as of 6/30/26

The trades listed herein encompass all transactions executed under the strategy during the second quarter (April 1 – June 30). This update is intended to offer a complete and transparent reflection of trading activity for second quarter of 2026.

1. Early-Quarter Re-Risking: Improving Breadth and Income Diversification

We began the quarter by selectively increasing risk exposure as geopolitical conditions showed signs of stabilization and market breadth improved.

We exited McCormick after concluding that the investment case had deteriorated. The company’s legacy volume growth profile had weakened, organic growth was increasingly price-driven, and the announced Reverse Morris Trust transaction with Unilever Foods introduced significant integration, leverage, and international execution risk. Given the combination of weak underlying volume trends and a more complex strategic path, we no longer believed the risk/reward fit the portfolio.

We also trimmed McDonald’s and TJX after strong performance and position-size drift, while reallocating capital toward Alerian MLP ETF (AMLP). The increase in MLP exposure improved portfolio yield and added real-asset income exposure at a time when energy and inflation risks remained elevated.

As geopolitical concerns eased further, we trimmed iShares 0-3 Month Treasury Bond ETF (SGOV) and increased equity exposure through JPMorgan Equity Premium Income ETF (JEPI), JPMorgan Nasdaq Equity Premium Income ETF (JEPQ), Vanguard International High Dividend Yield Index Fund ETF (VYMI), and Taiwan Semiconductor. These trades were designed to re-risk the portfolio in a measured way while remaining aligned with the income mandate. JEPI and JEPQ provided lower-volatility equity participation with attractive income characteristics, VYMI added global dividend diversification, and Taiwan Semiconductor increased exposure to AI infrastructure and advanced semiconductor manufacturing.

We also exited Wells Fargo and trimmed Williams. The Wells Fargo exit reflected concerns around earnings quality and spread monetization relative to peers, while the Williams trim was primarily valuation-driven after strong performance.

2. Mid-Quarter Rotation: Shorter Duration, AI Infrastructure, and Higher-Quality Income

The second phase of the quarter focused on improving the strategy’s balance between income generation, duration risk, and secular growth exposure.

Within fixed income, we reduced duration by trimming Vanguard Intermediate-Term Corp Bond Index Fund ETF, Simplify MBS ETF, and intermediate government exposure, while increasing Vanguard Short-Term Corporate Bond Index Fund ETF, Janus Henderson AAA CLO ETF, and JPMorgan Income ETF. This reflected our view that inflation risk remained underappreciated and that the Fed’s ability to cut rates could be constrained. The fixed income sleeve was positioned to maintain carry while reducing sensitivity to long-rate volatility.

We also initiated TE Connectivity and ExxonMobil. TE Connectivity added exposure to AI-adjacent industrial demand, data centers, electrification, aerospace/defense, and transportation content growth. ExxonMobil added high-quality energy exposure with potential benefits from upstream production, liquid natural gas, refining, chemicals, and firmer commodity prices.

We trimmed AstraZeneca as a risk-management trade. This was not driven by a deterioration in the company-specific thesis, but rather by position-sizing discipline after the holding had grown larger within the strategy. We continue to view AstraZeneca as a high-quality healthcare compounder but believed it was prudent to normalize exposure and redeploy capital toward areas with more immediate upside or stronger portfolio-construction benefits.

During May, we reinitiated Broadcom and later added NVIDIA. Broadcom provided a dividend-eligible way to increase exposure to AI networking, custom silicon, and infrastructure software. NVIDIA became more compatible with the strategy following its ~25x dividend increase and expanded capital return profile, while remaining one of the clearest beneficiaries of AI infrastructure demand across compute, networking, software, and full-system AI factory deployments.

We modestly trimmed Prologis to help fund the NVIDIA purchase. This was also not a change in our underlying view of the company. We remain constructive on Prologis given its high-quality industrial real estate portfolio, strong balance sheet, and long-term positioning around logistics, e-commerce, supply-chain modernization, and data-center-adjacent infrastructure demand. However, given the opportunity to add a higher-conviction AI infrastructure beneficiary that now fit the strategy’s yield framework, we believed a modest Proloigis Inc. trim was appropriate.

We also initiated SAP, funded by a reduction in utilities exposure. SAP gave the strategy a yield-eligible way to participate in the enterprise AI transition. While software sentiment remained challenged, we believed SAP’s ownership of mission-critical enterprise data, workflows, permissions, and system-of-record infrastructure positioned the company to benefit from AI adoption rather than be displaced by it.

3. Late-Quarter Discipline: Reducing Uncertain AI Spend, Harvesting Gains, and Managing Volatility

Late in the quarter, we shifted from adding risk to refining risk as both market performance and valuation risk rose substantially in June. The strongest parts of the market had moved quickly, and we became more focused on valuation, position sizing, and portfolio volatility to hold true to our strategy’s mandate.

We trimmed and ultimately exited Meta, reallocating capital toward companies with clearer linkages between AI capex and revenue realization. Our concern was not Meta’s core franchise, which remains strong, but rather the uncertainty around the return on its very large AI infrastructure and internal model spending program. We preferred to own clearer monetizers of industry-wide AI capex, including Broadcom, NVIDIA, and Alphabet-related exposure.

We added GOOGM, a mandatory convertible security tied to Alphabet, which provides a high-coupon equity-equivalent exposure and complements the portfolio’s existing Alphabet position. We continue to view Alphabet as well positioned across AI monetization through Search, Cloud, YouTube, and its internal TPU ecosystem.

We also initiated Flowserve while exiting Accenture and Xylem. Flowserve offered a more attractive combination of valuation, self-help, aftermarket growth, energy security, power, nuclear, and water infrastructure exposure. Accenture was exited due to concerns that AI could pressure the traditional consulting and outsourcing model over time. Xylem was exited because the original quality-compounder thesis had become more dependent on delayed growth reacceleration and continued margin execution.

Finally, we trimmed Taiwan Semiconductor, Caterpillar, and Applied Materials after strong performance. These were not thesis changes. We remain constructive on AI capex, semiconductor equipment, industrial power demand, and data-center-related infrastructure spending. However, after significant appreciation and rising valuation risk, we believed it was prudent to harvest gains and reduce exposure modestly.

We redeployed a portion of capital into Microsoft, where we see a more attractive risk/reward within technology. Microsoft offers a more defensive business mix, strong enterprise distribution, embedded AI monetization opportunities, and strategic exposure to leading frontier AI platforms. We believe the stock provides a better balance of quality, valuation, AI optionality, and volatility control than some of the more extended AI infrastructure beneficiaries.

2Q Attribution Snapshot

All performance is preliminary and unaudited

- For the second quarter, the Tactical Income Composite returned +4.59% Gross / +4.46% Net versus +6.24% for the benchmark*, underperforming by about 165 basis points.

- Year-to-date the Tactical Income Composite returned +3.33% Gross / +3.07% Net versus +4.39% for the benchmark*, underperforming by about 116 basis points.

- Yield on the Portfolio as of 6/30/26 was 4.3%.

- The standard deviation of the portfolio was 5.5%.

- Relative attribution was primarily driven by security selection, which detracted approximately 116 basis points. Asset allocation detracted approximately 38 basis points, while foreign exchange allocation contributed approximately 2 basis points.

- The strategy’s equity sleeve contributed approximately +435 basis points to absolute return, but the benchmark’s* equity sleeve contributed approximately +583 basis points, resulting in an active drag of roughly 148 basis points.

- Average exposures during the quarter were approximately 47.3% equity, 49.2% fixed income, 2.3% cash, and 1.2% commodities.

- At quarter-end, allocations had shifted to approximately 48.8% Equity, 47.8% Fixed Income, 2.4% Cash, and 1.0% Commodities, versus 41.4% Equity, 54.0% Fixed Income, 3.2% Cash, and 1.3% Commodities at the end of 1Q26.

- Top five positive security-level contributors included JP Morgan Nasdaq Equity Premium Income (+78bp), Cisco (+41bp), Applied Materials (+38bp), Taiwan Semiconductors (+35bp), Caterpillar (+28bp)

- Bottom five detractors included FT Vest Gold Strategy Target Income (-16bp), SAP (-11bp), McDonalds (-8bp), AstraZeneca (-5bp), Flowserve (-5bp).

- At the sector level, Information Technology and Consumer Discretionary were the largest drags due to non-ownership in non-dividend yielding companies.

- The modified duration of the fixed income Portfolio sleeve was 3.45 with an average credit rating of A.

Market Outlook

Looking ahead, we believe the market environment remains constructive but increasingly selective. The second quarter demonstrated that risk appetite is still strong, particularly around AI infrastructure, semiconductors, power, industrial capex, and companies tied to the physical buildout of the AI economy. However, we also believe the easy phase of the trade is behind us. Valuations have moved higher, investor expectations have risen, and the market is becoming more discriminating about which companies can convert AI spending into durable earnings and cash flow.

Within equities, we remain constructive on AI exposure, but we are focused on quality, valuation, balance sheet strength, and income eligibility. We want exposure to the AI buildout, but not at any price and not in a way that compromises the strategy’s yield and volatility objectives. That means continuing to emphasize companies with clear monetization paths, strong free cash flow, shareholder return, and identifiable links to infrastructure demand. It also means avoiding or reducing exposure where AI capital allocation is less certain or where the business model itself may be disrupted by AI.

We also believe market breadth can continue to improve, but leadership is likely to rotate more frequently than it did during the most concentrated phase of the AI trade. Industrials, energy infrastructure, global dividend equities, and select financials can continue to play important roles in a diversified income portfolio, particularly if nominal growth remains resilient and capital spending broadens beyond a handful of mega-cap technology companies.

In fixed income, we expect duration management to remain important. Inflation risk has not disappeared, fiscal pressure remains elevated, and policy uncertainty is likely to persist. We continue to prefer a flexible approach that combines high-quality carry, shorter-duration credit, securitized income, and selective intermediate-duration exposure when compensation is attractive. We do not believe duration should be treated as a static benchmark* exposure in the current environment.

Most importantly, the quarter reinforced the distinction between Tactical Income and an unconstrained 40/60 benchmark*. In strong momentum-led markets, particularly when leadership is driven by non-yielding or very low-yielding equities, the strategy may lag the broad benchmark*. However, we believe the strategy’s objective remains clear: generate competitive total return while maintaining diversified income, managing volatility, and preserving the flexibility to adjust as market conditions change.

We remain focused on building a portfolio that can participate in upside, produce income, and avoid becoming overly dependent on any single macro outcome or market leadership cohort. In our view, the opportunity set remains attractive, but the next phase will require greater discipline, more active risk management, and continued focus on income durability.

Sincerely,

The Hilton Tactical Income Investment Team

*Benchmark = 40% SP500 TR Index / 60% Bloomberg Intermediate US Govt/Credit TR Index Value Unhedged

Important Disclosures:

Hilton Capital Management, LLC (“HCM”) is a Registered Investment Advisor with the US Securities Exchange Commission. The firm only transacts business in states where it is properly notice-filed or is excluded or exempted from registration requirements. Registration as an investment advisor does not constitute an endorsement of the firm by securities regulators nor does it indicate that the advisor has attained a particular level of skill or ability.

The views expressed in this commentary are subject to change based on market and other conditions. The document contains certain statements that may be deemed forward looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. Sources include: Bloomberg and INDATA (our portfolio accounting and performance system). There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

The S&P 500 Total Return Index, often referred to as SPX TR, is a version of the S&P 500 index that includes both capital gains and dividends. Unlike the standard S&P 500 Price Return Index (SPX), which only reflects changes in stock prices, the SPTR reinvests dividends paid by the companies in the index, providing a more comprehensive measure of investment performance. We believe that this makes it a better benchmark for evaluating the actual returns an investor might receive.

The Bloomberg Intermediate US Government/Credit TR Index Value Unhedged Index is a broad-based benchmark that measures the non-securitized component of the Bloomberg US Aggregate Index with maturities less than 10 years. It includes: investment-grade, US dollar-denominated, fixed-rate Treasuries, government-related securities, and corporate bonds. The "Total Return (TR)" aspect means it includes interest income and price appreciation. "Unhedged" indicates that it does not use currency hedging, which is relevant for international investors.

The composite performance information contained herein is unaudited, was calculated by HCM and is shown on both a gross-of-fee and net-of-fee basis. The performance results herein include the reinvestment of dividends and/or other earnings, and the net-of-fee performance results are shown net of the actual advisory fees paid by the client accounts in the HCM Tactical Income Composite. In addition, actual client accounts may incur other transaction costs such as brokerage commissions, custodial costs and other expenses. Accordingly, actual client performance will differ, potentially materially, particularly given that the net compounded impact of the deduction of investment advisory fees over time will be affected by the amount of the fees, the time period, and the investment performance. For additional information about the composite, please contact us - info@hiltoncm.com

All investing involves risks including the possible loss of capital. Asset allocation and diversification does not ensure a profit or protect against loss. Please note that out- performance does not necessarily represent positive total returns for a period. There is no assurance that any investment strategy will be successful. All investments carry a certain degree of risk. Dividends are not guaranteed, and a company’s future ability to pay dividends may be limited.

Additional Important Disclosures may be found in the HCM Form ADV Part 2A, which can be found at https://adviserinfo.sec.gov/firm/summary/116357.